Last week, I wrote a couple of posts about the relationship between energy prices and US recessions. The second one had this graph:

I observed that

Before 1973, energy prices were not terribly volatile, were generally declining, and seem to have nothing to do with recessions. After 1973, energy prices are much more volatile, and there is a strong association between energy price spikes and recessions, with all recessions having an associated spike just before or in the early stages of the recession, and only one prominent spike lacking an associated recession (that in 2005).Several readers objected to this on the grounds that I was overemphasizing the role of energy relative to other commodities. Commenter Nick G, for example, wrote:

The most obvious cause of the regime shift is the peaking of US domestic oil supply (the green curve on the right scale), causing a shift to the US being heavily dependent on importing oil, and therefore at the mercy of OPEC control of the global oil supply.

You could begin to tease out the cause and effect relationships by doing the same analysis for other commodities that are associated with the classic booom-and-bust of commodities in the business cycle. A good one might be copper. I think you'll find a very similar set of charts, which suggests that the case for oil causing recessions isn't quite a strong as one might think.I would certainly agree that a "steel shock" for example, could in principle cause a recession. If for some reason there were suddenly to be considerably less iron and steel available than the economy had been expecting, producers could not, in the short term, adapt very readily except by producing less stuff. Particular models of cars or trucks currently in production require a set amount of steel, current building codes demand a certain amount of rebar in concrete, buildings currently under construction were designed some time ago and probably cannot be redesigned on the fly to use fewer steel girders, and so forth. And so if we were faced with a sudden reduction in the available steel, as a simple accounting matter of the physical commodity, the economy must produce fewer finished goods (since the great bulk of goods have some steel in). In the longer term (over a few years), the economy could adapt - products could be redesigned to use less steel and more of other commodities, and then the "steel efficiency" of the economy would go up, and more finished goods could be made from less steel.

So from this short-term-shock perspective, the difference between oil and steel is less due to the different ultimate physical role they play in the economy (energy versus matter), than it is to the fact that the sources of iron ore are diversified and not unduly concentrated in a single politically unstable region as oil is. Also, iron is present in extremely large amounts in the earth's crust, whereas oil is a very minor component of the crust that only arose in certain very special and limited geological circumstances, such that the total supply available to the economy is finite enough to matter greatly in the current century.

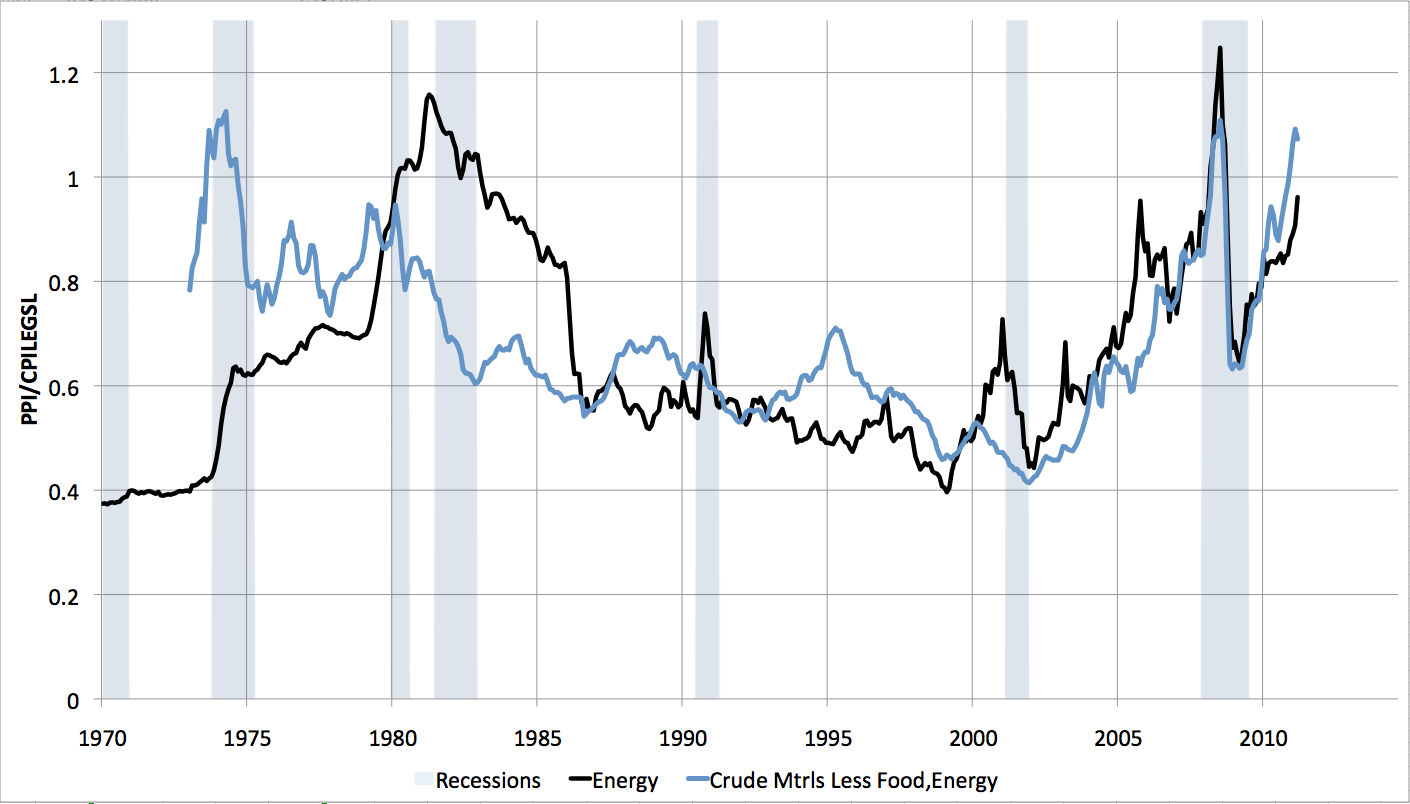

To get a more empirical sense of the situation, I cast around on the BLS website for producer price indexes for a while, and eventually came up with the "Producer Price Index for Crude Nonfood Materials Less Energy" as an index that incorporates a broad range of commodities but does not directly incorporate energy itself. I then followed the same procedure as here, of dividing this out by the CPI less energy to get a sense for how the commodity prices were changing after factoring out general changes in the price level (which are largely under the control of the central bank). That picture looks as follows:

Here the black line is energy, and the blue line is the other commodities. I have rescaled the blue line so that the two have the same average over the period since 1973 (the PPI crude commodities data only goes back to then, so we cannot see what things were like before the 1973 oil shock).

I make a few observations (which are not original to me). First is that there is a noticeable change in regime after the 2001 recession. Prior to that, energy prices and other commodity prices correlate weakly, but afterwards, they correlate strongly. You can see this even more clearly in scatter plots:

The left is the pre 2002 data in which there is basically very little correlation - R2 is 6% - while the right is the data from 2002 on which exhibits a strong linear relationship with an R2 of 80%. So it appears that a new thing is happening in the world to create a relationship between commodity prices generally and energy prices in particular.

However, if we just focus on the earlier region of the graph before 2002, it looks like this:

You can see that here the other commodities are less strongly associated with the onset of recessions. The more typical pattern is that commodities peak somewhere in the middle of the cycle and then decline (eg 1995 or 1988). With 1973 as the obvious exception, there are not the sharp increases in commodity prices right near the beginning of recessions that characterize energy prices - for example, look at the behavior of the two curves in 1991.

I take this to mean that in this period, other commodities were not generally in tight enough supply to play an important role in slowing growth or causing recessions.

However, since 2002, we have this:

I would guess that this much stronger correlation is due to the tremendous surge in the growth of China, and to a lesser extent other emerging markets, which is putting strain on the ability of many resource extraction industries to mine the planet fast enough to keep up. So it could be that other commodities are now in tight enough supply to be a material brake on growth in coming years.

8 comments:

One could also speculate that financial engineering plays a role. The glut of savings all over the world looking for higher returns has shifted from real estate to commodities, that are known to be in more or less limited supply. This puts these markets in line with the other financial markets which all track recessions pretty closely. Just a stray idea.

Burk:

I suspect you're right that that's a factor.

Searching for "______ price manipulation" will yield all manner of fruit; wheat, steel, copper, oil, you name it. Oil gets more publicity via Matt Taibbi and Mike Masters testifying before congress, as well as being far more blatant to consumers that the rest, but there's no shortage of pieces on traders driving up the prices of other commodities.

Chris Cutler presented his conspiracy of manipulation of Brent at TOD; JD used to go on about B-Wave being rigged etc etc.; also how all other commodities were rising in lockstep, and that can't be for real, can it?

Obvious counterpoint was a chart of iron ore prices, which isn't traded in futures, yet rose inexorably 2000-2008 anyway. I gave up at some point; markets intervene to an extent short term, but fundamentals obviously provide the...fundament? No one could go long for a decade straight.

Your conclusions here are very interesting. Commodities perhaps just aren't around in sufficient supply to keep markets supplied; the "spare capacity" of steel etc just isn't there. Maybe? Good luck quantifying that one.

Today I did some serious pruning on the blogs I subscribe to. I without hesitation kept your blog because it is so refreshing to read data based analysis on important issues rather than just opinions. Thank you very much for your efforts.

With regard to today's topic I wonder if the recent correlation of commodities with energy can be attributed to "peak everything". For example, we now mine low grade ore bodies which requires more energy. And we need more energy and resources of all types to produce energy from low eroei sources like tar sands. And we fish for scarce tuna with big fast boats burning lots of diesel. etc. etc.

Rob:

I'm glad I made your cut.

I did wonder the same thing - whether energy was sufficiently important in the cost structure of commodity production that energy prices were starting to bleed through into other commodities from the cost side. A little googling found a handful of graphs of cost structure for mining operations and it looked like energy was only 10-15% of their operation. So it didn't seem promising that this was the main thing going on. I didn't explore in any more detail at this time.

That's just the cost of mining, leaving aside the cost of shipping - this link states that shipping was equivalent to 21-57% of the spot price of iron ore at delivery to China, depending on source: Iron Ore Prices.

Jeff Rubin made the enigmatic statement in his book that with crude >$100/bbl bunker fuel becomes >50% of a commodity price. Never caught a ref for this and always meant to corner him at his blog about that.

>I wonder if the recent correlation of commodities with energy can be attributed to "peak everything".

-0-

If this is true; why hasnt the 'gold' price of things moved as much as the $?

To me, there are such things as the commodity cycle and inflation of the central reserve currency (USD) certainly can inflate many commodities at the same time.

Otherwise; agree with everything KLR said.

I have an observation. Even at The OIL Drum, perhaps the most unique characteristic of oil is rarely mentioned, namely, that it already consumes a substantial fraction of GDP (~5%). I believe the total cost oil cannot double, nor can the cost of any substitute reach this point. It does not seem much of a stretch to suggest the price of energy started causing recessions when these increases began to have a major effect on marginal income.

Post a Comment