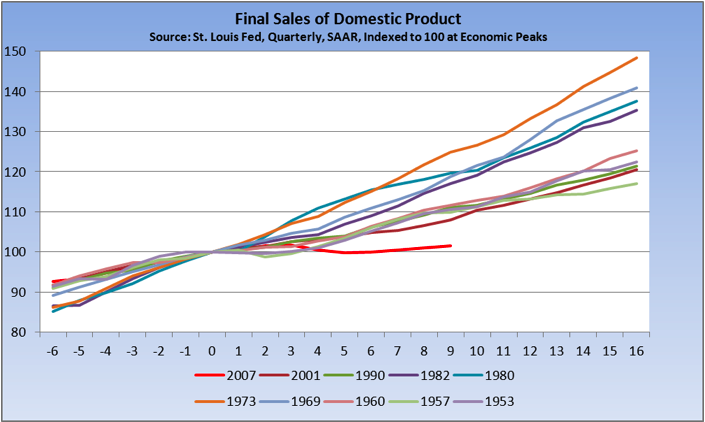

Buried in this post by Invictus over at the Big Picture, is the above amazing graph, showing final sales of domestic product following various economic peaks immediately prior to recessions. This is in real (ie inflation adjusted) terms, and I double-checked a couple of the curves myself from the raw data since I was having a little trouble believing it. Obviously, one thing going on here is that US economic growth has generally not been as strong in the last couple of decades as it used to be back in the 50s and 60s.

But the larger issue is that basically there is no real recovery following the great recession.

Paul Krugman also has a very interesting post looking at what the inflation data looks like if you don't use the year-over-year changes normally used (which are a lagging indicator during turning points), but instead look at the month-over-month changes (annualized), and just fit a trend-line to them to cancel out noise. For one particular inflation measurement, he gets:

So this is deleveraging at work. And of course deflation is the worst possible thing to happen when you are trying to deleverage, as it makes the real value of debt steadily greater over time, making it even more difficult to repay.

Krugman's snarky comment at the end of the post inspired me to go reread Ben Bernanke's famous 2002 speech Deflation: Making Sure "It" Doesn't Happen Here. In it, he argues that there are always ways for the central bank to inject money into the economy and prevent deflation. In discussing why Japan was nonetheless unable to prevent deflation from occurring, Bernanke said:

First, as you know, Japan's economy faces some significant barriers to growth besides deflation, including massive financial problems in the banking and corporate sectors and a large overhang of government debt. Plausibly, private-sector financial problems have muted the effects of the monetary policies that have been tried in Japan, even as the heavy overhang of government debt has made Japanese policymakers more reluctant to use aggressive fiscal policies (for evidence see, for example, Posen, 1998). Fortunately, the U.S. economy does not share these problems, at least not to anything like the same degree, suggesting that anti-deflationary monetary and fiscal policies would be more potent here than they have been in Japan.So far, both factors seem to be just as operative in the US in 2010 as they were in Japan in 2002. It will be interesting to see if policy-makers are able to mount a materially better response as the situation grinds on.

Second, and more important, I believe that, when all is said and done, the failure to end deflation in Japan does not necessarily reflect any technical infeasibility of achieving that goal. Rather, it is a byproduct of a longstanding political debate about how best to address Japan's overall economic problems. As the Japanese certainly realize, both restoring banks and corporations to solvency and implementing significant structural change are necessary for Japan's long-run economic health. But in the short run, comprehensive economic reform will likely impose large costs on many, for example, in the form of unemployment or bankruptcy. As a natural result, politicians, economists, businesspeople, and the general public in Japan have sharply disagreed about competing proposals for reform. In the resulting political deadlock, strong policy actions are discouraged, and cooperation among policymakers is difficult to achieve.

7 comments:

I have a feeling the entire argument against QE has yet to properly see the light of day. We suffer because none of us can read Japanese depriving us of their monetary debates.

My guess is that it risks undermining faith in the currency at a time when people have become more sensitive to its capacity to hold value longer term.

So, now that we have all the problems that Bernanke said we didn't in 2002 - "massive financial problems in the banking and corporate sectors and a large overhang of government debt" - then what does that mean? Certainly we still don't have government debt on the same level as Japan, but part of the reason they ended up there was through bailout policies where all the money got sucked up by the financial sector.

Basically, what Bernanke said was, "we don't have these problems now, and even if we did we could theoretically fix them as long as politics doesn't get in the way". 8 years later, we have those problems, America is in a state of political deadlock, etc. Except we don't have trade barriers and such, so our domestic industry has been eviscerated, unlike in Japan.

I think the problem is that you CAN'T just "inject money" into a system like this, at least not by traditional means. Due to the huge amount of bad debt, the money all gets sucked up by the financial structure. The only solution I can see is writing off most of these debts, and creating policies that prevent money from being sucked up in the financial system. The problem is that every real thing now is covered with so many layers of financial paper, getting money to real investments is nearly impossible.

I still think Salman Khan's idea of letting old banks fail and creating new banks with no liabilities in their place is a better idea than trying to reinflate the value of the old banks. Sadly, it's politically unfeasable. Our best case is a "lost decade", our worst case is a true depression.

Great blogpost ot read here on the slowdown coming by Edward Hughes:

http://edwardhughtoo.blogspot.com/2010/07/is-there-global-economic-slowdown-in.html

My one comment regarding the data is that the GDP numbers get benchmarked once every few years and the effect is quite significant (the path taken after the 2001 recession, for one, would've looked differently). I would've liked to see the graph at the top done with original growth estimates, not the final triple-benchmarked result.

I expect multiple recoveries each followed by a recession for net no-growth over the next decade. As we are in a depression, not a recession, that is what one would reasonably expect. It's the end of historic debt and credit cycle that goes back at least 25 years, with a blow off phase that started at least 10 years ago. Surprisingly, I am more optimistic than most energy economists as I believe the world will actually incrementally find a way to adopt coal and gas more widely, as oil supply (in real terms) ebbs away. Thus, the two restraints I see on the OECD economy come from the Debt overhang, and the problem of transition (more than the problem of oil supply per se).

G

Gregor:

Yeah, in a way, the debt situation makes the oil supply situation less urgent -- it will be easier to get enough supply to cover depressed demand -- though in the long term, that's probably a bad thing, as we will be slower to make the adaptations we need to make the transition away from oil.

Post a Comment